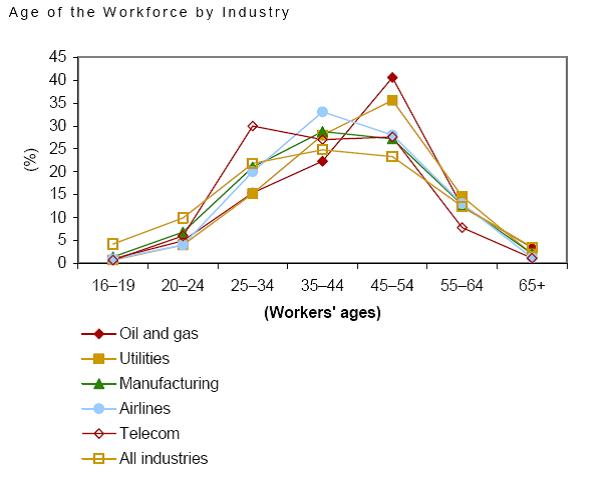

I saw this graph the other day. It plots the age distribution of various industry workforces. It suggests that the Oil and Gas industry has the highest age workforce.Telecom has the youngest age workforce and airlines are sort of middle of the pack

Oil's workforce age distribution reflects a higher mean than others for several reasons: (i) operating experience is the most important thing in this industry and this comes with age, and (ii) the oil industry has a clubishness about it that supports the notion of "tenure"...almost in a professorial way, and (iii) America's youth has had a declining interest in pursuing a career in oil.

One could argue that the oil industry will someday have a manpower issue. By looking at the graph one would conclude that this industry is not alone. An average human may find comfort in the notion that "all industries" are in trouble. But the relative magnitude of distress to be experienced by each of these industries compared in the graph is, in my opinion, substantially different.

As US labor has learned from its highly-capable manufacturing competitors in China (among other locations), substitution of one workforce for another is not overly disruptive to the manufacture of many types of products. It is, in fact, encourage for those products based on labor-dollar efficiency. This has the positive result to US labor of allowing those workers substituted to pursue a higher complexity calling and thus higher real earnings. However, maybe not every labor sector depicted is in the same boat "manufacturing"....what's different about oil?

Difference: The location and extraction of hydrocarbon-based fuels is highly scientific and multi-disciplinary. In addition, this science is augmented substantially by accumulated experience. As a result, workforce substitution is not that easily performed. That's why we and the Russians raced after so many German scientists near the end the end of WWII (See Werhner Von Braun..."Operation Paperclip"). They had the best rocket scientists in the world. If these scientist had been lost to another country...our space program would have lagged for years. Same thing in Oil. When this workforce starts retiring en masse we are going to have some problems unless we can increase the work capabilities of those left standing to super human levels.

The current day rates for offshore drilling rigs are at all-time highs. There are currently nearly 90 offshore drilling vessels under construction (www.coltoncompay.com) that can be deployed over the next 4 years. While this may seem to be a solution to declining production curves of today's reserves...my question is this..."who is going to staff these rigs...and who is going to teach those intended to staff these rigs how to operate them?"

This is a picture of a drilling control room.

A drilling rig is a highly-technical piece of equipment. Imagine, as an example, an additional 90 space shuttles showing up off the assembly line ready for our use...imagine the incremental infrastructure and training required just to get an additional shuttle operating at the same time as our other active space shuttles. I would think that the value of knowledgeable shuttle crews would go up substantially. Likewise, owners of drilling rigs would pay substantial market premiums to rig crews in order keep their rigs active....so as to make the interest payments to the bank that loaned for their construction. While this will, in fact, attract more oil industry labor pool applicants...it will not solve the implicit labor shortage for a long time.

A drilling rig is a highly-technical piece of equipment. Imagine, as an example, an additional 90 space shuttles showing up off the assembly line ready for our use...imagine the incremental infrastructure and training required just to get an additional shuttle operating at the same time as our other active space shuttles. I would think that the value of knowledgeable shuttle crews would go up substantially. Likewise, owners of drilling rigs would pay substantial market premiums to rig crews in order keep their rigs active....so as to make the interest payments to the bank that loaned for their construction. While this will, in fact, attract more oil industry labor pool applicants...it will not solve the implicit labor shortage for a long time.So my conclusion is that the degree of labor shortage problem indicated by the graph is much greater than meets the eye. What is really going to happen on the rigs is that the better crews are going to go onto the better rigs. The older rigs are going to have to live with the "less-better" crews. As a result, the drilling contractors with the older fleets are going to have to buy the new rigs to get the better crews back...and they will pay premiums to do this.

Furthermore, the increased number of rigs will scatter to drilling plays all over the world rather than reflect a few geographic concentrations (as was the case in the Gulf of Mexico for so many decades) which exacerbates the problems of training crews and managing projects. As gravity attempts to pull the energy industry from its historical epicenter in Houston, Texas...what are companies based here going to do to prevent this? How will they manage against increased competition?